Content

Three methods that companies use to value inventory are FIFO, LIFO, and weighted inventory. Under GAAP, companies are required to disclose information about their accounting choices and their expenses in footnotes. Both GAAP and IFRS aim to provide relevant information to a wide range of users. However, GAAP provides separate objectives for business entities and non-business entities, while the IFRS only has one objective for all types of entities. In addition, the economic environment continues to change, with companies facing increased uncertainty.

Which is better US GAAP or IFRS?

By being more principles-based, IFRS, arguably, represents and captures the economics of a transaction better than GAAP.

IFRS includes the distinct category of investment property, which is defined as property held for rental income or capital appreciation. Investment property is initially measured at cost, and can be subsequently revalued to market value. The IFRS Foundation works with more than a dozen consultative bodies, representing the many different stakeholder groups that are impacted by financial reporting. Is allowed in the income statement only under the GAAP framework, whereas IFRS does not consider such an item. Method Of LIFOLIFO is one accounting method for inventory valuation on the balance sheet.

Cash flow statements

David has helped thousands of clients improve their accounting and financial systems, create budgets, and minimize their taxes. Although the merging efforts were made on financial performance reporting, it seems that the main problems lie with the difference in the method of the U.S. The IFRS is more vibrant and is constantly being revised in response to an ever-changing financial environment.

Companies that are involved in foreign activities and investing benefit from the switch due to the increased comparability of a set accounting standard. However, Ray J. Ball has expressed some scepticism of the overall cost of the international standard; he argues that the enforcement of the standards could be lax, and the regional differences in accounting could become obscured behind a label. He also expressed concerns about the fair value emphasis of IFRS and the influence of accountants from non-common-law regions, where losses have been recognised in a less timely manner. International Financial Reporting Standards are a set of accounting standards that govern how particular types of transactions and events should be reported in financial statements.

IFRS vs US GAAP Differences

On 8 September 2022, the IASB published an Exposure Draft of proposed amendments to its ‘International Financial Reporting Standard for Small and Medium-sized Entities’ . The IASB has now released a webcast offering deeper insights into the proposals on financial instruments included in the ED. When expanded it provides a list of search options that will switch the search inputs to match the current selection.

us accounting vs international accounting refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms are legally separate and independent entities. Over a decade ago, it was believed that the whole world would likely adopt the Generally Accepted Accounting Principles . At the point in time, the International Financial reporting Standards was only about ten years old. Currently, it is anticipated that the U.S. will converge its GAAP with the international IFRS, leaving behind only a modified IFRS.

Critical Differences Between IFRS and US GAAP

However, despite the care taken by translators and the oversight provided by translation review committees, translation problems exist. In some cases, words and phrases used in English-language accounting standards cannot be translated into other languages without some distortion of meaning. The IFRS Foundation is a not-for-profit, public interest organisation established to develop high-quality, understandable, enforceable and globally accepted accounting and sustainability disclosure standards. GAAP standards require organizations to write down the market value of their fixed or inventory assets, and this write-down amount cannot be reversed even if the asset’s market value increases over time. US foreign listed companies can now reconcile their financial statements according to IFRS instead of GAAP.

Is accounting different in different countries?

Because accounting standards originated within countries as they sought to standardize commerce within their borders, international accounting does not exist per se but is instead a collection of those individual national methods. Each country follows its own set of generally accepted accounting standards.

If you’re a preparer, it may help you identify areas to emphasise in your financial statements; if you’re a user, it may help you spot areas to focus on in your dialogue with preparers. The treatment of developing intangible assets through research and development is also different between IFRS vs US GAAP standards. Costs in the development phase may be capitalized based on certain factors. On the other hand, US GAAP generally requires immediate expensing of both research and development expenditures, although some exceptions exist. When the IASB sets a brand new accounting standard, several countries tend to adopt the standard, or at least interpret it, and fit it into their individual country’s accounting standards.

ENHANCING RELATIONSHIPS AND COMMUNICATIONS WITH OTHER NATIONAL STANDARD SETTERS

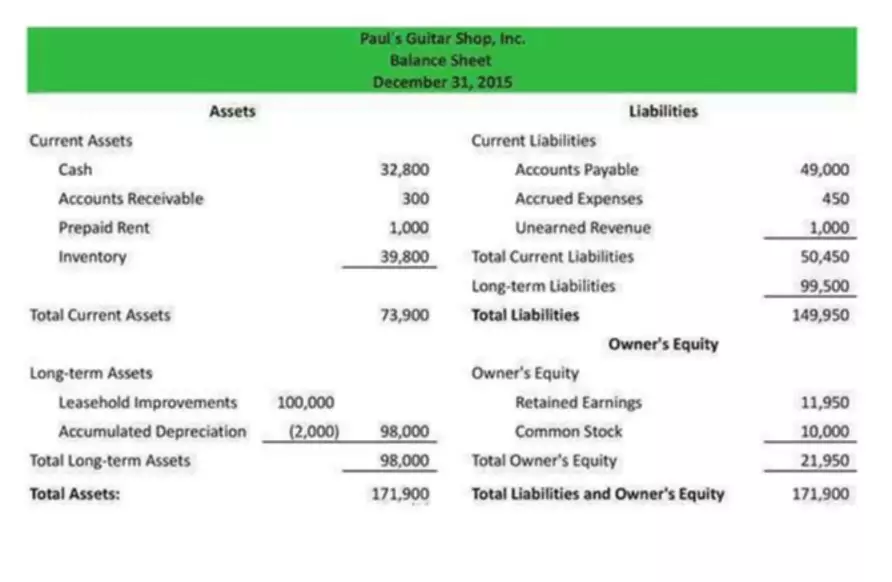

The way a balance sheet is formatted is different in the US than in other countries. Under GAAP, current assets are listed first, while a sheet prepared under IFRS begins with non-current assets. Accounting standards are critical to ensuring a company’s financial information and statements are accurate and can be compared to the data reported by other organizations. Under GAAP, development costs are expensed as incurred, with the exception of internally developed software.

- While the approaches under GAAP and IFRS share a common framework, there are a few notable differences.

- Once a good’s been exchanged and the transaction recognized and recorded, the accountant must then consider the specific rules of the industry in which the business operates.

- One of the reasons IFRS does not support LIFO is that it’s impossible to achieve accurate inventory flow using this method.

The main objective of accounting standards is to disclose a company’s financial health to investors, creditors, lenders, contributors, and other key stakeholders, which helps those parties make strategic business decisions and invest in new opportunities. The concept of convergence first arose in the late 1950s in response to post World War II economic integration and related increases in cross-border capital flows. Over 144 countries use IFRS, making IFRS the global standard for accounting. The majority of G20 counties use IFRS apart from China, India, and Indonesia, which all have national accounting standards that resemble IFRS. In GAAP, acquired intangible assets (like R&D and advertising costs) are recognized at fair value, while in IFRS, they are only recognized if the asset will have a future economic benefit and has a measured reliability.