As millennials increasingly enter the housing market, yet another concern looms: are you willing to get a home having education loan loans? With respect to the National Association regarding Realtors (NAR), plenty of home buyers has pupil obligations. Indeed, a complete 41% out-of earliest-time home buyers carry out. So if you have been operating underneath the assumption you to student education loans imply you cannot end up being a homeowner, reconsider!

Before racing with the mortgage mentor, regardless if, you will find several things you must know. Some tips about what you must know throughout the student education loans and purchasing property.

Perform college loans apply to to get property?

Because there is noted, you can naturally purchase property having figuratively speaking – and several people carry out. The following logical question for you is, just how do your fund effect your home to shop for sense?

The clear answer: college loans make a difference your debt-to-money ratio, credit rating, and also the amount it is possible to cut getting a down-payment, and all of these items therefore can affect the borrowed funds price and financial you might qualify for. Let us after that crack you to off.

Debt-to-earnings proportion

Anytime you check out get property, you can easily explore cost management with both your own Realtor and your home loan advisor. The greater loans you’ve got in proportion toward income, the fresh quicker house you might basically afford. To put it differently, student loans can get mean that you be eligible for a less expensive family than simply you or even you can expect to pay for together with your income top.

Debt-to-money height, otherwise DTI, will be based upon your own monthly debt payments – and therefore covers sets from auto money so you’re able to playing cards. Normally loan providers favor a DTI of thirty-six% otherwise smaller, which have 43% being the high DTI a debtor can have when you’re nevertheless being qualified to possess home financing. However, which number might be higher with authorities-recognized mortgages (like the FHA).

Which have an educatonal loan does not prevent you from taking recognized having a home loan. Education loan costs might be calculated like any almost every other debt whenever trying to get a home loan, shows you experienced Financial Mentor Beam Garville. Like many motivated payments, education loan money rating counted inside the what is called the debt-so you’re able to money-proportion getting choosing how much cash off a mortgage we’re going to meet the requirements to have. If you have a payment stated for the a credit history, that is the percentage that will be utilized.

Credit rating

Would student education loans apply at credit ratings? They’re able to. Exactly how undoubtedly you have taken the loan obligation yet will has influenced your credit score. If you’ve produced the student loan commission punctually each month, you should have a high credit score. If you have missed money – if you don’t defaulted on the the all of them – your get might be lower. A decreased credit rating function high mortgage prices, which means that large monthly premiums.

Education loan repayments is actually reported to your credit agencies like other debts and have an impact on a credit rating; when the discover later payments it’ll have a bad feeling to your a credit history, while paid down since the arranged it’ll have a confident impression into the a credit score, notes Garville.

Downpayment

Typically, its better if home owners shell out 20% of the house’s really worth at closing. This down-payment, as the entitled, assists in maintaining financial pricing and you will monthly obligations realistic and you may allows property owners to eliminate the other commission out of Personal Home loan Insurance policies (PMI). Millennials who may have had to repay its finance whenever you are carrying out of from the entry-level services try not to have a lot of money on the financial when it comes time to invest in a property.

not, first time household buyer programs generally allow homebuyers to place off only 5% at closure – and this may not be since big problematic since you think it is.

Can i pay financial obligation before buying a property?

Potential home buyers commonly wonder whether or not they should pay-off the student education loans otherwise get a house. There isn’t any right respond to here, specifically once the quantity of obligations you’ve got, how fast you could potentially pay it back, additionally the style of domestic we want to be eligible for all the impression so it choice.

- The reason of many homeowners decide to buy a property if you’re expenses of student loans is due to looking at its complete loan picture. Each year, the price of homes is likely to rise, since carry out rates of interest. For folks who pay-off $20,000 inside student obligations, although cost of your possible household increases $20,000 across the 2 years you’re rescuing, in that case your complete loan burden hasn’t shifted much.

- When you have highest-desire funds, even in the event, it might sound right to pay such away from first.

- Given that that have a larger down payment can assist maintain your financial speed lower -and even half of a portion speed is equate to tens and thousands of dollars over the life of your loan – it will make a great deal more sense to keep towards downpayment alternatively of one’s education loan.

- For individuals who slow down to purchase a home, you could be spending so you can book rather. After you spend the mortgage, that is equity you are free to continue. After you lease, you might be however paying off home financing – but this is your landlords.

To order a house that have college loans into the deferment

If you have deferred student education loans – which means youre back in college, on the military, otherwise is show financial adversity (government figuratively speaking have been along with deferred getting on account of COVID) – you may be curious just how this influences what you can do to shop for a home.

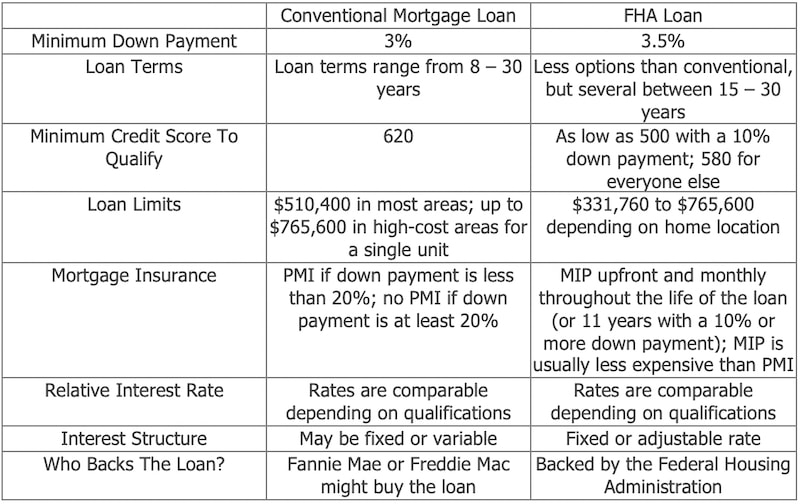

If you are choosing an enthusiastic FHA financing: Typically, FHA loan providers must play with step 1% of your student loan equilibrium within the online personal loans TN monthly premiums when determining whether the borrower match the maximum personal debt to money ratio away from 43%.

Put differently, for those who are obligated to pay $20,000 in figuratively speaking, loan providers usually envision 1% of these – or $200 – getting your own monthly loan duty, though you’re not expected to pay some of it down nowadays.

Traditional funds are often more easy than FHA direction, so if you carry a top education loan debt, you might find finest achievement around.

Having college loans and purchasing a home is common

College loans are only a type of loans, and financial obligation by itself doesn’t keep some one back away from to invest in homes: in reality, people to buy house involve some brand of obligations, whether it’s student loans, vehicle payments, or credit card bills. What you need to perform is actually keep the credit score upwards, check your debt-to-income ratio to see how much home you really can afford, and you may communicate with an experienced, better Agent on which variety of house can match your requires and you may finances.